Meet the Fastest

Mortgage Lenders in Houston

There are plenty of qualified mortgage lenders in Houston, TX. But only one of them can be the fastest mortgage lender in America. Welcome to Zeus Mortgage Bank. We aren’t like the other mortgage lenders in Houston. We close all of our mortgage loans faster than our competition. Most of the time, it’s not even close. As a mortgage lender, we prioritize speed because we know that when it comes to closing on a home or an investment property, timing matters. That’s why our Houston mortgage lending experts contact every loan applicant as quickly as possible to go over their mortgage options in detail.

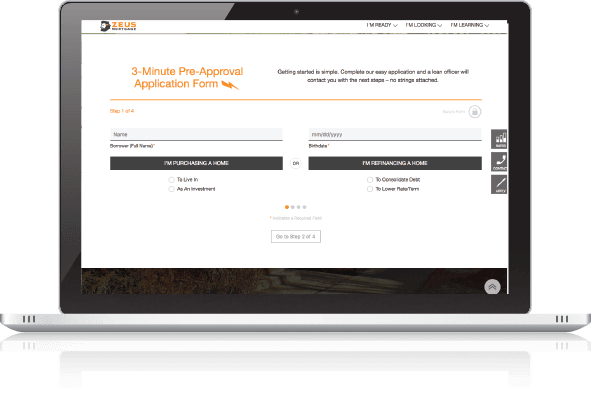

Apply in Just 3 MinutesIt All Starts With Our

Fast and Easy 3-Minute

Mortgage Loan Application

It only takes 180 seconds to tell Zeus Mortgage Bank everything we need to know to get started processing your mortgage loan in Houston. You won’t have to wait weeks to receive your mortgage loan terms. Zeus Mortgage Bank loans take only days from loan application to closing. We pride ourselves on being the fastest mortgage lenders in Houston, TX, and we ensure that no one in Houston or anywhere else in the United States can provide a conventional mortgage loan faster than Zeus Mortgage Bank. Not convinced? Fill out our 3-minute mortgage loan application now—there’s no obligation to you!

Apply in Just 3 Minutes

Zeus Mortgage Bank Isn’t Just Fast. We’re Flexible, Too!

Our mortgage lender services are the best in Houston. Once we receive your mortgage loan application, our lending experts will contact you shortly to discuss your options. Even if you’ve been denied for a mortgage loan in the past, Zeus Mortgage Bank will do our due diligence to find a lending method that will work for you. That’s the Zeus Mortgage Bank difference: We’re the only mortgage lender in Houston willing to go above and beyond for every applicant with no strings attached. That’s the level of customer service that borrowers expect in Texas, and Zeus Mortgage Bank considers it only neighborly to provide it to every person who fills out our fast, simple 3-minute mortgage loan application. What are you waiting for? Fill out our 3-minute application now and see how much time and money three minutes could save you over those other Houston mortgage lenders!

Apply in Just 3 MinutesCLIENT GOSSIP

WARNING: This video contains unscripted testimonials from actual Zeus Mortgage clients.

WARNING: This video contains unscripted testimonials from actual Zeus Mortgage clients.

As one of the top ten real estate brokers in Houston for almost a decade, I have worked with hundreds of big and small mortgage lenders. It’s very rare for a mortgage lender to be ready to close before the buyer or seller are ready. When Zeus says they will finish the loan before the buyer is finished packing, these guys mean it! They really are the fastest mortgage lender in America!

WARNING: This video contains unscripted testimonials from actual Zeus Mortgage clients.

We completed our home refinance and it went well, no problems. It has been a pleasure and I’d like to tell your boss how terrific and professional you are! You explain the process and are very prompt and responsive. I hope your boss knows what an asset you are! I will highly recommend anyone I know to call you at Zeus Mortgage!

WARNING: This video contains unscripted testimonials from actual Zeus Mortgage clients.

I just wanted to tell you that you are a pleasure to work with. If there is someone I can tell at your company ( a boss or someone higher up) how exemplary your work and communication skills are, I would love to do that for you. I hope you have a great Friday!

WARNING: This video contains unscripted testimonials from actual Zeus Mortgage clients.

Best Mortgage Experience ever! Very detailed, but great to work with. Really know their stuff. Thanks Zeus and Amanda!

Thank you, Trey Narendorf, Lynn Espinosa and the Zeus team for all of your help during the refinance of our home! Looking forward to the new house payment with the lower interest rate! We close on Monday.

I highly recommend Zeus they are very professional and are there to help you get exactly what you are looking for. I just refinanced and I am very very pleased….thank you.

- ZEUS IN THE NEWS